Are you intimidated by investing and don’t know where to start? Most people think you need deep pockets, ample free time, and a Wall Street education to start investing. I’m excited to tell you – none of that is true!

In fact, about 80% of American millionaires are self-made. They started with nothing, and learned to save and invest money from the ground up. Anyone can do it, and so can you.

The goal of investing is to simply buy assets that will increase in value over time. In this post we’ll be covering a basic five-step plan to start investing for beginners. It’ll include setting a budget, how and where to open accounts, and what assets to invest in. We’ll also cover a bunch of common investing questions towards the end.

Learning to invest might not be the most fun topic in the world, but I promise you it is worth it! Once you nail the basics and demystify some of the complexity, it turns out that building wealth is actually quite easy.

Why you need to start investing NOW!

Have you ever said to yourself, “I’ll start investing when I make more money.” Perhaps you’ve been concerned about market volatility as a result of recent current events (like during the COVID-19 global pandemic). It’s not that your hesitancy doesn’t make sense. The truth is that putting your investing journey on the back burner could cost you more than you realize.

In fact, experts estimate that ~40% of folks have experienced a financial loss due to procrastination. By waiting to invest, you could be missing out on potentially lucrative financial gains. Consequently, the timing of when you start investing could make a bigger impact on the amount you end up with than how much money you actually invest over time.

When it comes to investing for beginners, the earlier you start the better. The sooner you begin the longer your money will be working for you.

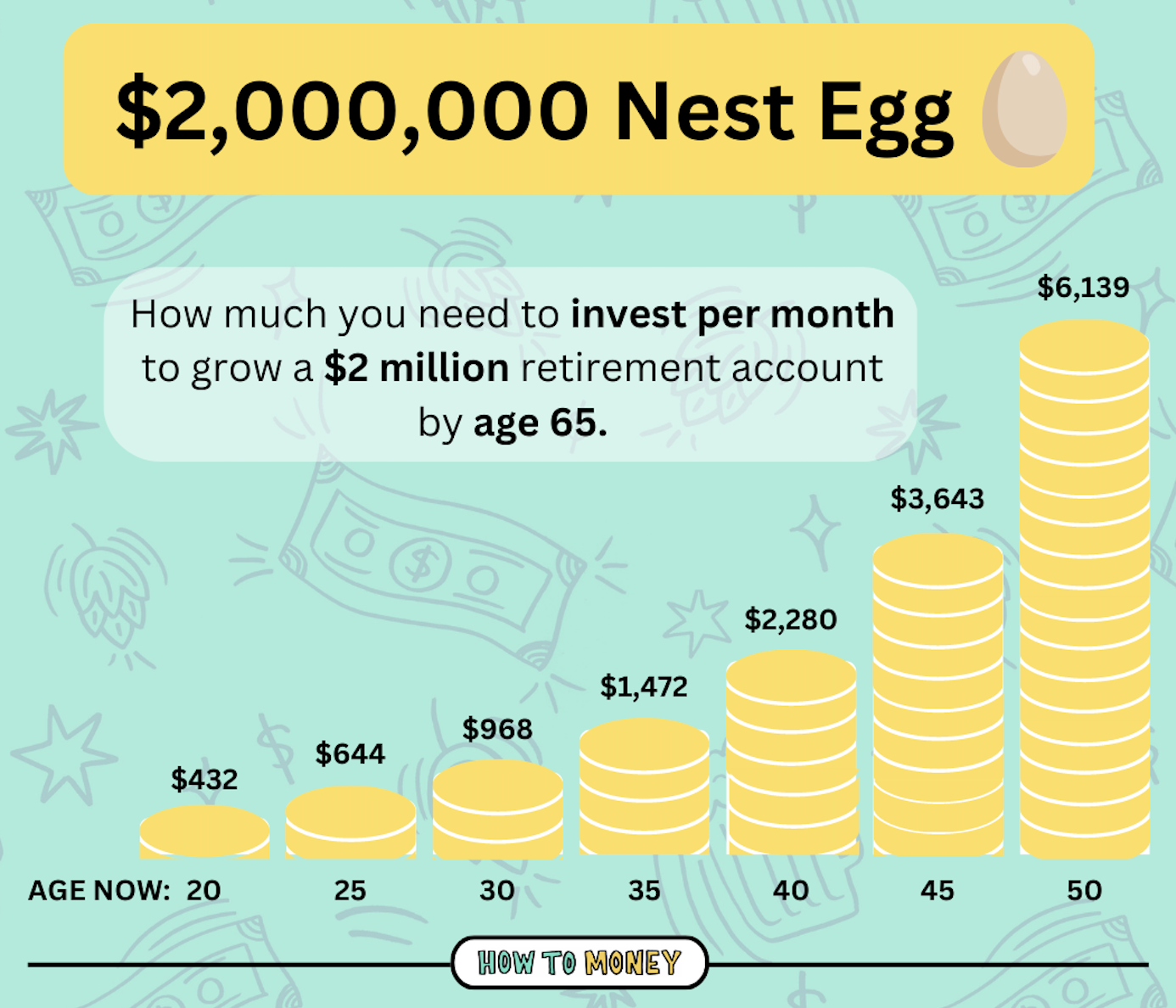

For example, check out the chart below. For a 20 year old to build a $2 million retirement portfolio, they would only need to save and invest about $432 per month. But for a 30 year old starting with nothing, that number is more than doubled!

For any older folks out there, this may seem disheartening. But while getting started early is a massive help, it’s also never too late to start investing for beginners!

The Power of Compound Interest

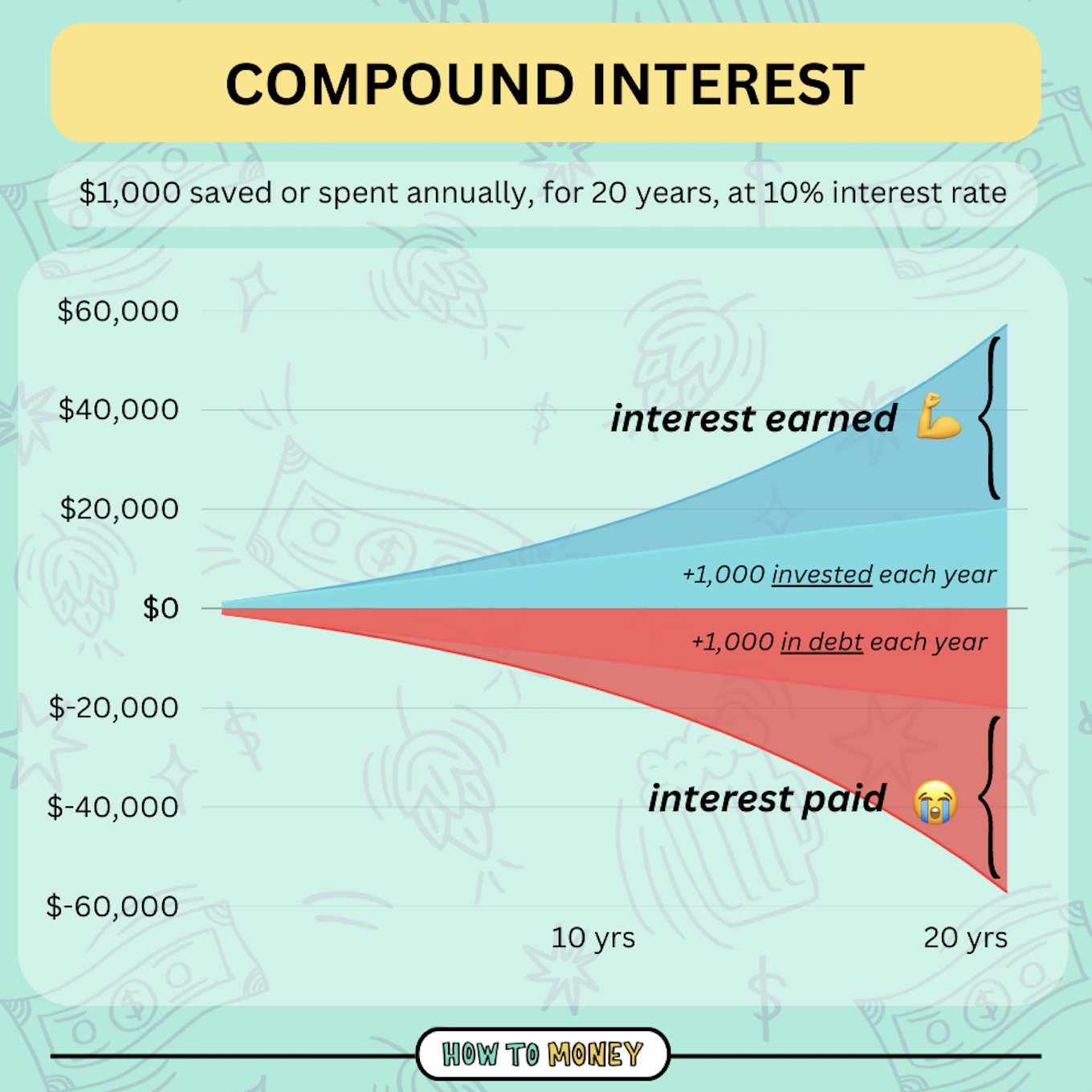

The excitement of investing is that even a small account balance can grow into a large pile of cash over time. That’s because of the power of compounding interest. Compound interest is making money on top of the money you’ve already earned. You’re not just earning interest on your principal balance; your interest earns interest!

Here’s how it works: Let’s say you have $2,500 in a savings account that earns 5% in annual interest. In year one, you’d earn $125, giving you a new balance of $2,625. In year two, you would earn 5% on the larger balance of $2,625, which is $131.25—giving you a new balance of $2,756.25 at the end of year two.

This might seem like small numbers, but believe me – things really add up over time.

One other thing to consider is that compound interest can work for or against you. Here’s an illustration of how someone saving $1,000 per year earns amazing interest! But someone spending/borrowing each year PAYS big interest.

Bottom line: Make sure compound interest is working for you, not against you.

When it comes to compound interest, the more time you have the better. The sooner you start saving and investing for retirement (or any other goal for that matter), the more time you’ll have to take advantage of the power of compounding. In a way, it’s kind of like free money.

Investing for Beginners – 5 Step Guide

Fortunately, there are countless ways to begin investing for beginners – with most of them requiring a minimal time commitment. Choose a strategy to get started investing depending on the amount you’ll invest, the time frames for your individual financial goals, and the level of risk that makes sense for you.

Here are some simple steps to help you get started on your investing journey:

1. Define Your Goals & Set Your Budget

As you start the process of investing, you’ll want to think about your goals so that you can determine a budget. Investment goals might include buying a house, funding your retirement, or saving for you or your child’s education. Remember, it’s only natural for your goals to change over time as your stage of life changes.

Most financial experts recommend investing 15% to 25% of your post-tax income. But before determining how much you want to set aside, take a close look at your monthly income and figure out how much money you have left over after paying all your expenses. I like to call this your margin. If you can only start with 5% to 10%, that’s OK – it’s better than 0%!

Starting small is better than failing to start.

It’s also important to mention that you shouldn’t start investing until you’ve got some cash on hand in a regular ol’ savings account. Establishing an emergency fund is vital before you start investing in the stock market. This is simply a fund where you set cash aside to make it available for an easy withdrawal – if needed. Establishing an emergency fund will act as a safety net in case you’re in a situation of having to sell off investments during a time of need.

2. Determine Your Risk Tolerance

While investing can produce great returns over time, it also comes with risk. In this case, risk is merely the potential for your investments to lose value. If you invest $1,000, it might be worth $850 at the end of the year. That sounds awful, right? On a short timeline, investing comes with real risk. The longer your investing horizon, however, the less risky that decision becomes.

As an investor, it’s up to you to decide how much risk you’re willing to take on.

For instance, a conservative investor usually has a lower risk tolerance and wants to put their money into investments with guaranteed returns. On the other hand, an aggressive investor commonly has a higher risk tolerance and is willing to risk more money for the possibility of better returns. The bigger the risk, the bigger the reward, etc.

Considerations such as age, investment goals, and income are generally used by financial advisors to help investors determine their risk tolerance. Once you determine your risk tolerance, you’ll have a clearer picture of what types of investment purchases you’re most comfortable with.

It’s important to note that there is a risk to not investing too. We’ve all seen the impact that inflation can have on our purchasing power. When your pay goes up by 3% a year but your grocery bill soars by 12%, that’s a tough pill to swallow. The persistent reality of inflation is a real risk to your money and investing helps you mitigate that risk.

*Time* Can Lower Your Risk

Taking advantage of time is one of the ways you can decrease your risk while increasing your reward. History shows that the longer you keep your money invested, the greater your chances of enduring any downturns.

When your earnings compound, your investment gains expand tremendously over time. Long-term investments are frequently thought to be less speculative and risky than short-term investments, as they are less likely to fluctuate in value in the short-term.

Let’s break down the secret sauce that makes investments less risky — time. As history has shown, if you invested in the stock market for one year, your chance of losing money would be greater than 25%. However, if you invested for 10 years, that percentage drops dramatically to 4%, and after 20 years to 0%.

*Diversification* Can Lower Risk

Another way to lower risk is diversifying your investments. This is like spreading your eggs across multiple baskets.

One hundred years ago, investors heavily relied on stock brokers and fund managers to advise them on which stocks/bonds would make up a diversified portfolio. But thankfully these days, with modern technology advancements, diversifying your investments is quite easy!

We’ll dive into diversification via index funds a little later on. And you’ll be happy to know that some of the broadest and most diversified index funds available also have the highest average returns over long terms.

3. Open an Investing Account (or several)

Now we’re going to talk about what type of accounts you can open and a little about how each one works. Ideally you want to start off with any accounts that have tax advantages, as minimizing tax savings can help your investments grow faster.

401(k) Retirement Accounts:

One of the most convenient ways to begin investing is through an employer-sponsored 401(k) plan (or 403(b) if you work for a nonprofit or government entity). It’s especially beneficial if your job offers a match, which is essentially free money.

Check to see if your employer offers any type of retirement plan. If so, it should be seamless to set up a deduction from your paycheck. All you’ve got to do is figure out how much you want to contribute and make it happen.

Benefits of a 401(k) or 403(b) plan:

- Paycheck deductions: Money is taken out of your paycheck *before* you get paid. This truly is a “set and forget” type of investing account. The more you automate your investments, the easier wealth building is.

- Tax Advantages: Traditional 401(k) plans reduce your taxable income for the years you are investing. Paying less in taxes means your money grows at a faster rate (even though you will have to eventually pay taxes, later)

- Employer matching: Some employers offer additional money if you contribute to your workplace retirement plan. If your work offers this, take advantage, ASAP!

- You are in control of the money! When you leave your employer, you can “roll over” the money or bring the account with you to another employer.

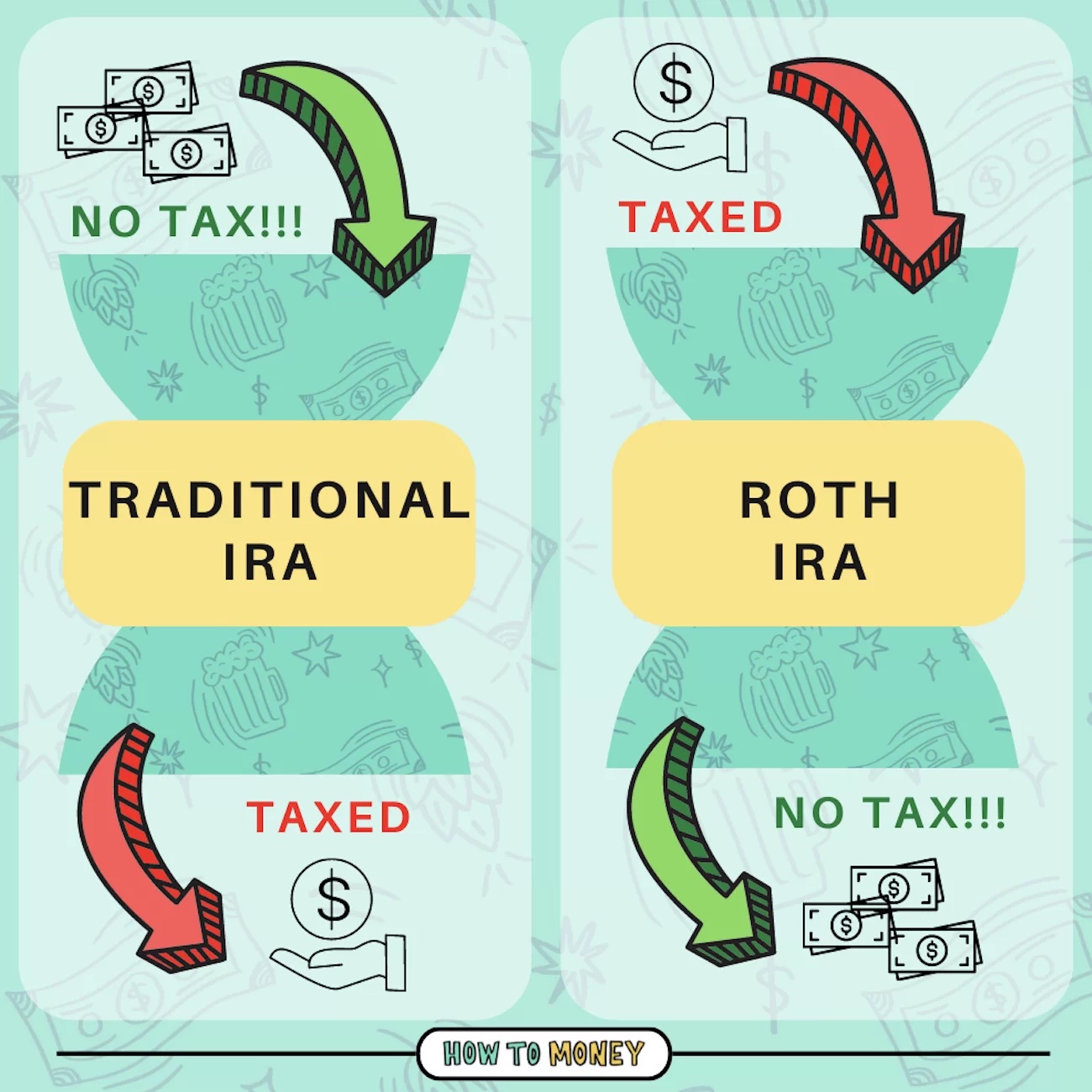

Traditional IRA and Roth IRA:

Another way to jumpstart your investing is through a personal retirement savings account, like an Individual Retirement Account (IRA) or Roth IRA. They’re offered by a variety of financial institutions and are simple to set up online.

We’ve written a great guide to help you decide whether a Traditional IRA or Roth IRA is better for you. One helps you save taxes now, the other helps you save taxes later…

- A Traditional IRA is comparable to a 401(k): You invest pre-tax money, let it grow over time, and pay taxes when you withdraw it in retirement.

- A Roth IRA allows you to invest after-tax income and then the money grows tax-free and is not taxed upon withdrawal.

- There are also specialized retirement accounts for self-employed workers such as SEP-IRAs, Solo 401(k)s, and SIMPLE IRAs.

Bonus: How to become a Roth IRA millionaire

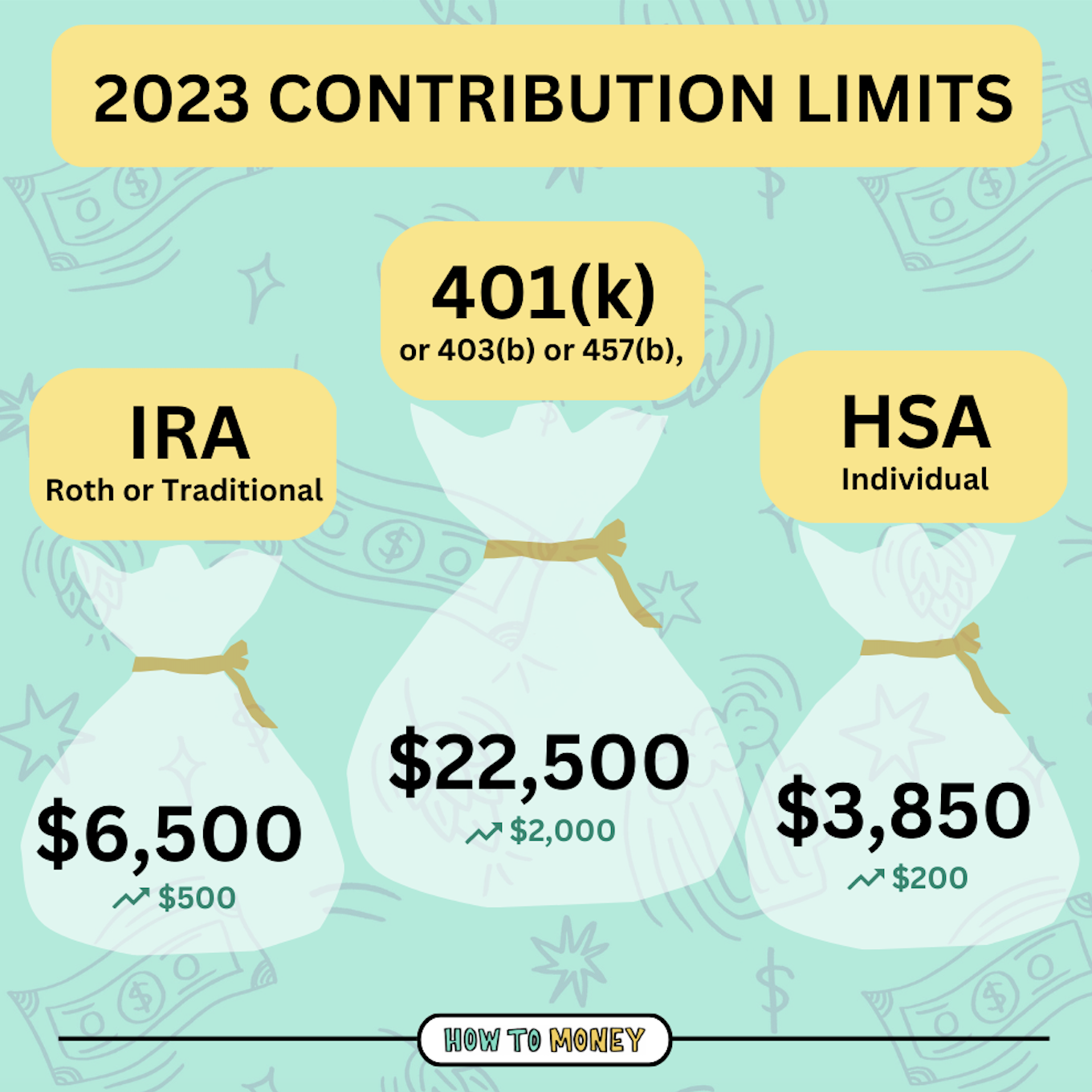

Contribution Limits (2023)

Be aware that the IRS limits the amount you can add to each of these accounts on a per year basis. Also, these limits tend to be adjusted yearly so be sure to check the account limits on your preferred plan to adjust your budget accordingly.

- For 2023, the 401(k)-contribution limit is $22,500 (before employer match) and $6,500 for an IRA.

- Older workers (those over age 50) can add an additional $7,500 to a 401(k) as a catch-up contribution, while an IRA allows an additional $1,000 contribution.

Income Limits – How much money you earn will determine your eligibility to contribute to a Roth or Traditional IRA. The IRS sets income limits that restrict high earners. The limits are based on your modified adjusted gross income (MAGI) and tax-filing status.

- Roth IRA income limits for the 2023 tax year are $153,000 (was $144,000 in 2022) for single filers and $228,000 ($214,000 in 2022) for married couples filing jointly.

- There are no income limits for Traditional IRAs – meaning you can contribute no matter how much money you earn. However, there are income limits for tax deductible contributions.

Brokerage Accounts

A brokerage account is another type of investment account that allows individuals to buy and sell things like stocks, bonds, mutual funds, and exchange-traded funds (ETFs). These accounts have no tax advantages, so we always recommend funding the above mentioned accounts first!

You can open a brokerage account online with little to no money up front in most cases. There is no limit on the number of brokerage accounts you can have or the amount of money you can put into your account annually.

Also, there should be no fee associated with opening an account. We recommend Vanguard and Fidelity mostly, as these are the largest brokers with no account fees. Modern “robo-advisors” are good options also. M1 Finance and Betterment are two of the best in that category. We’ll get into more detail about these low cost brokers below!

4. Buy Stocks/Bonds/Funds (Low-Cost Mutual Funds/ETFs recommended)

After you’ve decided where you are going to invest, now it’s time to choose what to invest in. First, let’s quickly review what stocks and bonds are:

- Stocks – A stock is a share of ownership in a single company that is publicly traded. Stocks can also be referred to as equities. Stocks can be purchased for a share price, which can widely range based on the value of the company.

- [RISK FACTOR] —> If your savings goal is 20+ years away (like retirement), it probably makes sense for a majority of your money to be in stocks. However, picking individual stocks can be complicated and time consuming. As a result, most people find that the best way to invest in stocks is to buy a giant basket of stocks via low-cost stock mutual funds, index funds, or ETFs [see below].

- Bonds – When you purchase a bond, you are providing a loan to a company or government entity. That company/entity then agrees to pay you back in a certain number of years and during that time you earn interest.

- [RISK FACTOR] —> Bonds are typically a lower-risk investment than stocks because you know the payback date and how much you’ll earn. But, over the long run bonds come with less upside compared to stocks. Depending on your age and your specific goals, bonds should make up either a larger or smaller percentage of your investment portfolio (less bonds for younger folks, more bonds for older folks).

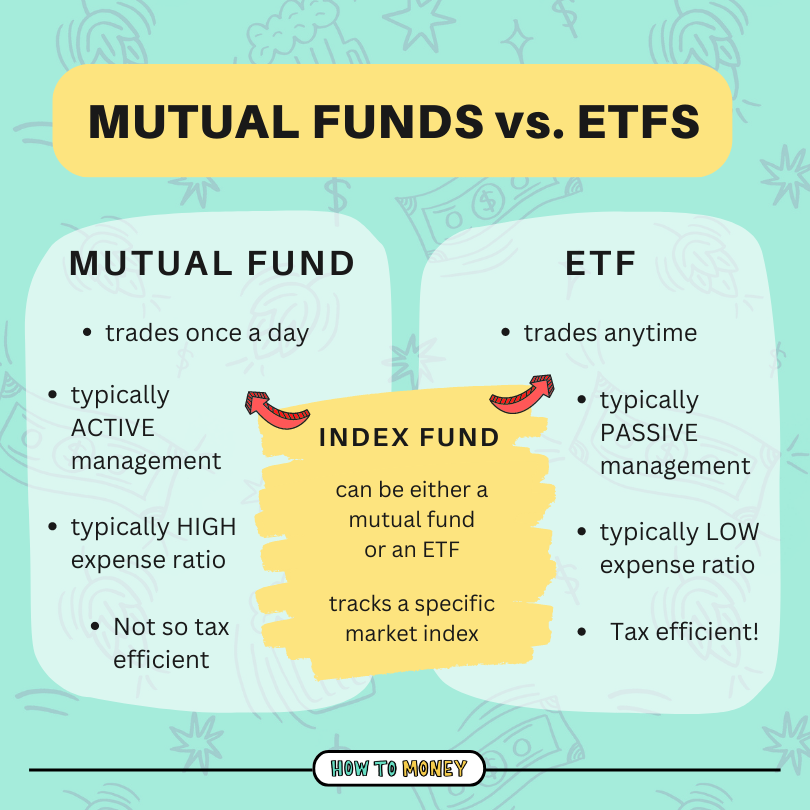

Now let’s talk about mutual funds and ETFs. Think of these as pre-packaged portfolios that contain hundreds (sometimes thousands) of stocks and bonds inside of them…

- Mutual Funds – A mutual fund is a mixture of investments packaged up and sold together. The idea is that you are mutually pooling your money with other investors to buy stocks, bonds, and other investments. Opting for a mutual fund allows you to bypass the work of picking individual stocks and bonds – instead, you’re buying a diverse collection in a single transaction.

- [RISK FACTOR] —> Because you’re spreading money across a massive pool of stocks, mutual funds are generally less risky than individual stocks. They are diversified!

- ETFs (exchange-traded funds) – Similar to a mutual fund, an ETF bundles many individual investments together. The difference is that ETFs trade throughout the day like a stock and are purchased for a share price. ETFs often track a certain sector, index, commodity, or other asset. An ETF’s share price is often lower than the minimum investment requirement of a mutual fund, which makes ETFs a good option for new investors or folks starting with small budgets.

- [RISK FACTOR] —> The biggest risk in ETFs is market risk. Meaning the markets go up and the markets go down. ETFs diversify risk by tracking different companies in a sector or industry in a single fund.

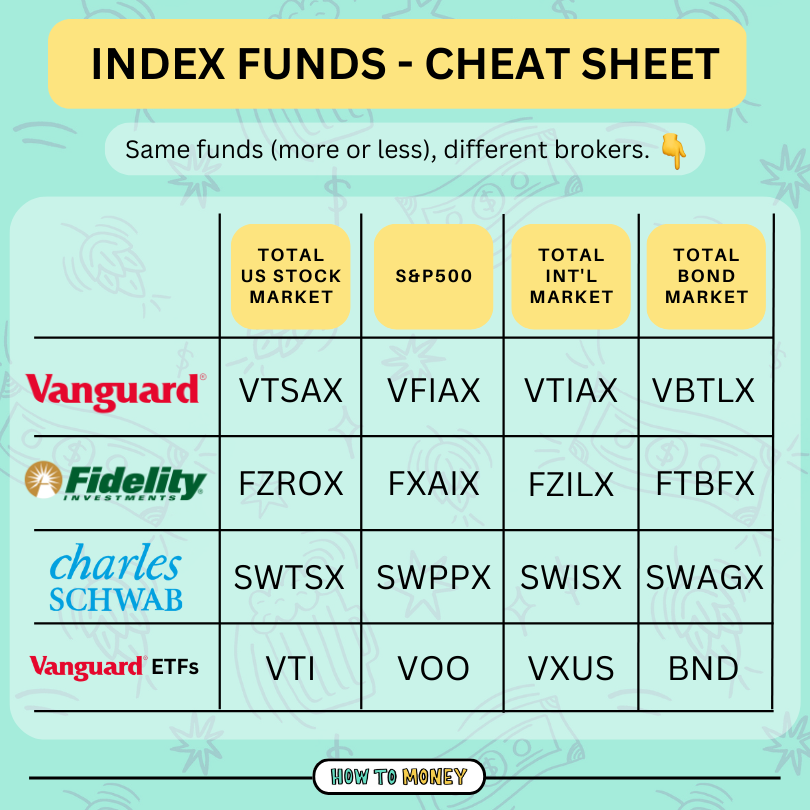

- Index Funds – As one of the easiest ways to invest (especially for beginners), index funds are ideal investments for long-term investors. They are a type of mutual or ETF fund that tracks the returns of a market index such as the S&P 500. When you take the index fund route, you are investing in all the companies that comprise a specific index, giving you a more diverse portfolio than if you bought individual stocks. Index funds have lower expenses and fees than actively managed funds and follow a passive investment strategy. The S&P 500 Index acts as a U.S. stock market benchmark. The index has posted a historic annualized average return of around 11.88% since its 1957 inception through the end of 2021.

- [RISK FACTOR] —> The odds that an index fund loses everything are very low because they are often so diversified. Index funds are known for outperforming actively managed mutual funds, especially when the low fees are taken into consideration.

Here are some of the largest and most common index funds we talk about on our podcast. (Also, we personally invest in these index funds mostly!)

5. Keep Investing (Dollar-cost averaging or automate)

Once you start investing, the key is to remain consistent over a long period of time to ensure that you are successful. Setting up automatic transfers so that they happen every two weeks or at the end of each month is the best way to ensure your success as an investor. Even modest contributions, when made regularly, can pay off in a big way over the long term.

Another method that may work best for you is called dollar-cost averaging. This practice involves investing a set dollar amount on a regular basis. Don’t worry about what’s happening in the market – just keep buying! This helps to create a disciplined investing habit in your life. By investing regularly but also spreading out your stock or fund purchases across time, you can use dollar-cost averaging to lessen the impact of volatility in your life. It’s also clearly easier to invest a little every time you get paid!

As you continue to grow as an investor, it’s more important to review the progress you’re making toward your goals over time, as opposed to tracking short-term highs and lows. Basically, don’t check your balance every month. That snapshot doesn’t offer enough information. What the market did in a particular day should have no impact on your life!

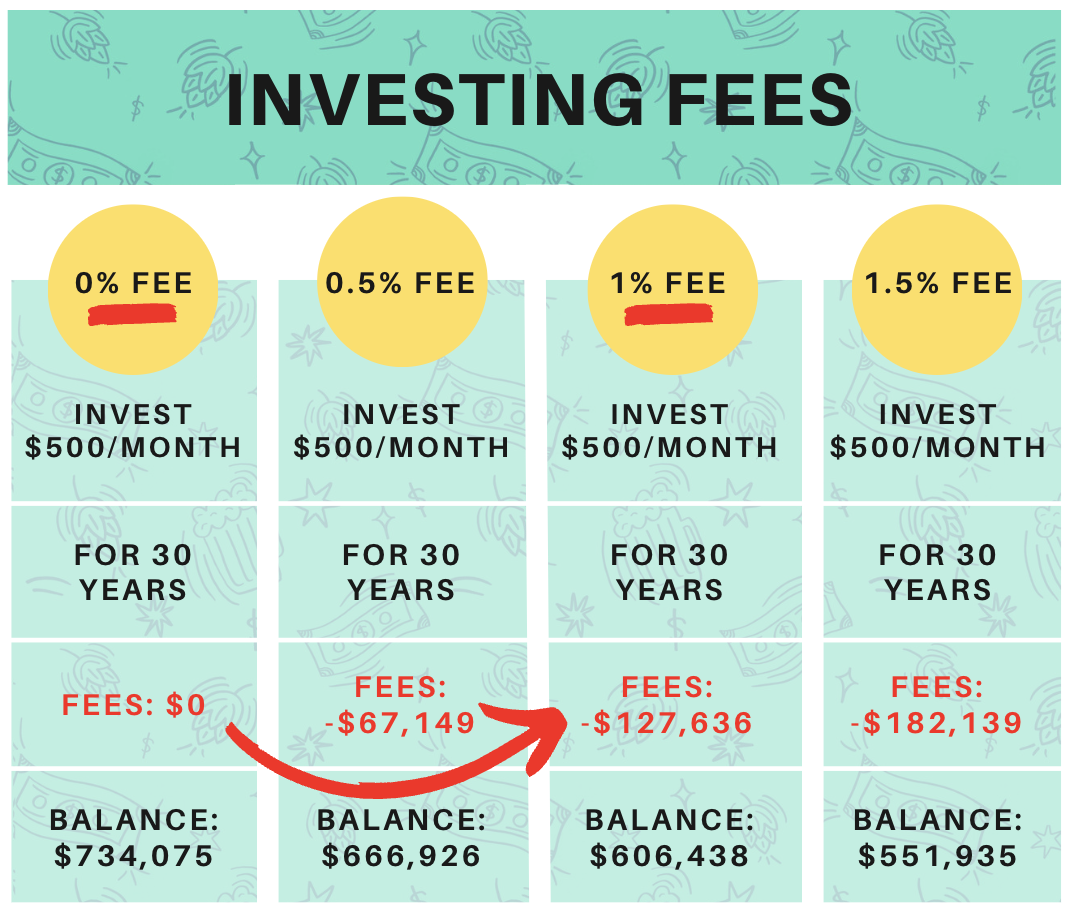

Avoiding Brokerage Fees

There’s no shortage of fees when it comes to investing! Common investment and brokerage fees include trade commissions, mutual fund transaction fees, expense ratios, sales loads, management or advisory fees, inactivity fees, research and data subscriptions, trading platform fees, paper statement fees, account closing or transfer fees, and 401(k) fees.

We HATE paying fees! They rob you of your investment returns.

Even a small brokerage fee can add up over the long haul. For example, you might think that a 1% commission doesn’t sound like much. However, if you invest for 30+ years that could eat away over $100,000 of your earnings!

You can avoid or minimize brokerage account fees by choosing an online broker that offers no account fees and commission-free trading. We’ve listed some in the FAQ below under Best Brokers for Beginners.

Another way to avoid fees is to passively manage your investments. Financial advisors can help solve complex problems within HUGE multimillion dollar portfolios. But for most folks (especially beginners just starting out) there is no need to involve an advisor. It’s not that they can’t be helpful. But it would be better to funnel the money you would have paid a professional into your investments instead!

Investing for Beginners FAQ:

Learning to invest can be overwhelming. But, YOU ARE NOT ALONE! Take your time and continue digesting bits of information here and there. After a while, you’ll start to pick up new terms and understand quickly.

Here are a bunch of beginner questions that might help…

Can you invest with just a little money?

Yes! Contrary to popular belief, you don’t need piles of cash to begin investing. You can start with as little as $1. For some folks, investing even $10 can feel like they’re stretching their budget too thin. But the amount of money you’re starting with isn’t as important as being financially prepared to invest money regularly over time.

Due to the power of compounding interest, investing is more about how much time you have, as it is about how much money you start with. So, once you’ve got that emergency fund in hand, even if you’ve only got a few bucks a month that you can contribute, go ahead and get started!

How much will you need for retirement?

The ability to truly “retire” will depend on many factors and everyone’s situation is unique. Of course, there is no shortage of benchmarks and guidelines for how much you need to retire on the internet. Some are more helpful than others.

One helpful rule of thumb is to work towards amassing 25x your annual expenses. For example, let’s say your annual spending is about $80,000 each year. This means you’ll want to save up about $2 million for retirement ($80K x 25). Studies have shown this is a safe estimate, also known as the 4% rule.

This may seem like an overwhelming number to save. But remember, compound interest is on your side. It’s the difference between saving and investing. Just begin making small and consistent contributions and you’ll be amazed how things grow over time.

What are the best brokerage accounts for beginners?

We recommend low-cost brokerage firms.

- Fidelity is awesome. Free to open accounts, free to buy most funds, and they also host a handful of ETFs with no or very low management fees!

- Vanguard is a fan favorite. The guy who founded Vanguard is the guy who invented index investing! His name is John Bogle, and he also authored The Little Book of Common Sense Investing which is a great book for beginners.

- Charles Schwab has been around for decades. They are the 3rd-biggest broker (behind the ones we already mentioned).

If you’re looking for a really slick interface, M1 is a great investing app. And if you’d like a bit more hand-holding while still keeping fees low, robo-advisors can be a great solution.

What are some common investing mistakes?

Being a good investor isn’t about picking skyrocketing stocks and having the perfect timing. In fact, it’s rarely about making the right moves, and more about avoiding the wrong ones.

When asked for their biggest investing mistake, most seasoned investors responded, “I should’ve started earlier.” So by just reading this post and getting started, you’re already taking action and avoiding further delay!

We’ve written extensively about why most people lose money in the stock market. But here’s a quick summary of common investing mistakes:

- Trying to time the market

- Paying too much in fees and commissions

- Lacking patience

- Individual stock picking (failing to diversify)

- Listening to “hot tips” from others

- Trading too much and too often

- Letting your emotions get the best of you

- Over-leveraging (borrowing money to invest)

What should I do when the stock market crashes?

As a long-term investor, you will live through several market crashes. But that’s OK, because you will also live through an equal amount of awesome market recoveries!

Market volatility is going to happen and can be created by unexpected economic news, changes in monetary policy, and political/geopolitical events. These are all things that are outside of your control. Just remember to stay calm and understand that this is most likely a temporary situation in the markets.

Here are a few things you can do to best prepare yourself during market volatility:

When the market crashes:

- Review your financial goals

- Build up your emergency fund

- Don’t panic sell

- Be opportunistic

- Consider investing MORE (crashes are excellent buying opportunities)

- Ignore the “sky is falling” news

Here’s a longer post about what to do when the stock market crashes!

Do I need a financial advisor?

If you are comfortable with money and have a basic understanding of investing, you’re probably fine managing your accounts on your own. The hardest part of investing is *waiting.* Picking accounts and buying index funds is quite simple, so there’s usually no need for an advisor (IMO!)

However, if you’re unsure of how to manage your finances or confused about how to make investments (even after reading this article), it could be worth hiring a financial advisor.

At different major milestones in your life, such as having kids, earning a promotion/large bonus, or inheriting money, you might want to consider chatting with an expert. It can be tough to know what to do when more money flows into your life!

Hiring advisors comes with a cost. And some of them might try to sell you costly products you don’t need. Our advice is to take your time selecting someone you trust. They should be a financial fiduciary (legally obligated to only recommend things in your best financial interest).

Still not sure whether you need to hire an advisor? Take a financial advisor quiz to help you determine your needs.

What is a Robo-Advisor?

Think of robo-advisors as apps that help manage your portfolio. They automate management so you can take a back seat when it comes to rebalancing, transferring money, or investing funds.

Robo-advisors can help create a diversified portfolio of low-cost mutual funds or ETFs that is suited to your needs after you provide some information about your goals, timeline, and risk tolerance. Most robo-advisors have fees, although some of them are free (that’s why we recommend M1 Finance – no fees!)

What about real estate investing?

If you think investing in the stock market is hard, times that by 10 and that’s how difficult real estate investing is to master. 🤣 All jokes aside, we recommend learning the basics and starting small with tax advantaged investing accounts before jumping into real estate.

That being said, real estate can be amazing for growing wealth. Investors earn money from rental revenue, appreciation, and some real estate investments offer tax advantages. Passive income, consistent cash flow, tax advantages, diversification, and leverage are all advantages of real estate investing.

There’s a big learning curve with investing in real estate. BiggerPockets is a great place to start – it’s the biggest online network of real estate investors. They also have a podcast that covers all types of ways to make money in real estate.

And here’s a HUGE post about the process to buy a rental property. It takes a lot of time and effort, but it’s all worth it in the end!

Despite all the advantages of real estate investing, there are some disadvantages. One of the most significant is a shortage of liquidity (hard to sell a property at the drop of a hat). A real estate deal can take months (or years) to research and close, as opposed to a stock or bond transaction, which can be finished in seconds.

Should I invest or pay off debt first?

Trying to build wealth while paying off debt is like swimming against a strong current. No matter how much effort you put into getting ahead, debt will continue to compound against you and pull you backwards.

This is why we created the 7 money gears. Think of it as an order of operations to follow. If you have high-interest debt, (credit cards, or anything above ~7% interest) you’ll want to prioritize paying that off before investing. **Except for 401(k) accounts or retirement plans that you get matching dollars from your employer.**

Not all debt is bad (check out good debt vs. bad debt examples here) so it really depends on your individual situation and numbers for when investing makes sense.

The Bottom Line

Beginning to invest can be the single wisest financial move you ever make, laying the groundwork for a lifetime of financial security and a peaceful retirement. Remember, you can’t “save” your way to retirement. You need to learn how to get your money to make more money – that’s where the power of compounding comes into play!

It’s never too late to start investing, no matter how old you are or where you are in life. You can’t undo what you’ve done or haven’t done, but you can change your future for the better. So, what’s holding YOU back? There’s no better time than now to start investing. Your future self will be grateful.

What Next? 3-Step Action Plan Moving Forward:

- Determine how much you can save/invest monthly —> Create a budget. Review your finances and your spending plan. How much can you invest on a monthly basis?

- Create a regular schedule —> Set up a regular transfers to your investment account and stick with it. Base the timing around when you get paid and when your bills are due.

- Increase your contributions over time —> It’s great that you can start investing with only $10 a week, but that’s not going to be enough long term. If you expect to reach your goals, you need to increase your investments over time. Work to creatively find ways to save more money to invest.